In April 2018 AIMA released a report entitled “Perspectives: Industry leaders on the future of the hedge fund industry”. Much of the content was dedicated to predictions forewarning of the technological arms race the industry has experienced in the past five years. Artificial intelligence. Machine learning. Big data. These previously only theoretical concepts have quickly evolved into practical applications, leading to the development of cutting-edge statistical and computational tools that are now part of mainstream investment strategies.

In order to generate alpha investment managers now invest heavily in technology, continuously evolving their processes to stay ahead of the curve. Use of artificial intelligence, machine learning, data acquisition, processing and analytics are all key elements for success. Tools are developed in-house by teams of software developers, mathematicians, physicists, computer scientists, and tailored to the specific needs of the investment strategy employed by each asset manager. Not all investment yields success, but when it does the results are bespoke, proprietary and often ground-breaking technological advances that provide managers with a competitive advantage over their peers. Even marginal gains can translate to significantly better investment performance, which in turn generate higher fees for managers.

Nevertheless, many investment managers still do not realise that in the UK this investment may qualify for R&D tax relief. Perhaps unsurprising given the R&D legislation and HMRC guideline are lengthy and difficult to interpret for a non-specialist. In this article we attempt to demystify some of the R&D concepts relevant for the R&D tax claim and outline the recent developments in this area.

What is R&D?

The definition of R&D can be summarised as follows:

- there must be a project;

- this project must seek to achieve an advance in science or technology;

- the particular activities of the project must either:

- directly contribute to achieving this advance in science or technology through the resolution of scientific or technological uncertainty; or

- be qualifying indirect activities.

The term ‘project’ is defined in HMRC Guidelines as: a project consisting of a number of activities conducted to a method or plan in order to achieve an advance in science or technology. It should encompass all the activities which collectively serve to resolve the scientific or technological uncertainty associated with achieving the advance, so it could include a number of different sub-projects. This definition needs to be considered in light of commercial activities and objectives of the investment manager carrying out R&D and its goals.

The Guidelines give the following meaning to an ‘advance in science and technology’: an advance in overall knowledge or capability in a field of science or technology (not a company’s own state of knowledge or capability alone). This includes the adaptation of knowledge or capability from another field of science or technology in order to make such an advance where this adaptation was not readily deducible.

An advance in science or technology may have tangible consequences (such as a new or more efficient investment platform) or more intangible outcomes (e.g. new knowledge or cost improvements for the investment manager).

From 1 April 2023 mathematical advances in themselves are treated as science for the purposes of HMRC Guidelines, whether or not they are advances in representing the nature and behaviour of the physical and material universe.

Just because science or technology was used in creation of a process, material, device, product, service or source of knowledge does not mean that it is R&D. There must be an advance in scientific or technological capability as a whole.

Data is an increasingly critical element for asset managers and the processes of collating, analysing and using it for investment decisions may impact funds’ performance. Developing platforms to optimise the data processing for investment management may qualify for R&D relief. Relevant part of the Guidelines in this case is that if a particular advance in science or technology has already been made or attempted by others but details are not readily deducible by a competent professional in the field (e.g. the details of the advance have been kept a trade secret), work by a competitor to achieve such an advance can still be an advance in science or technology. However, the routine analysis, copying or adaptation of an existing product, process, service or material, will not be an advance in science or technology.

Another important matter is that a project that seeks to make an appreciable improvement to an existing process, material, device, product or service through scientific or technological change will be considered as R&D. The improvement should be more than a minor or routine upgrading and should represent something that would generally be acknowledged by a competent professional working in the field as a genuine and non-trivial improvement.

The concept of scientific or technological uncertainty is discussed in the Guidelines and would exist when knowledge of whether something is scientifically possible or technologically feasible, or how to achieve it in practice, is not readily available or deducible by a competent professional working in the field. This includes system uncertainty. Scientific or technological uncertainty will often arise from turning something that has already been established as scientifically feasible into a cost-effective, reliable and reproducible process, material, device, product or service.

Uncertainties that can readily be resolved by a competent professional working in the field are not scientific or technological uncertainties. Similarly, improvements, optimisations and fine-tuning which do not materially affect the underlying science or technology do not constitute work to resolve scientific or technological uncertainty.

It is important to establish the technological baseline, then expand that to a level which a competent professional could achieve. Only once the second level is surpassed can activity qualify for R&D relief, summarised in the diagram below:

Some of the activities which directly contribute to R&D are:

- activities to create or adapt software, materials or equipment needed to resolve the scientific or technological uncertainty, provided that the software, material or equipment is created or adapted solely for use in R&D;

- scientific or technological planning activities; and

- scientific or technological design, testing and analysis undertaken to resolve the scientific or technological uncertainty.

Qualifying indirect activities are activities which form part of a project but do not directly contribute to the resolution of the scientific or technological uncertainty, some of the examples are:

- ancillary activities essential to the undertaking of R&D (e.g. taking on and paying staff, maintaining R&D equipment including computers used for R&D purposes);

- training required to directly support an R&D project;

- research (including related data collection) to devise new scientific or technological testing, survey, or sampling methods, where this research is not R&D in its own right; and

- feasibility studies to inform the strategic direction of a specific R&D activity.

Qualifying expenditure

Only the expenditure on the qualifying direct and indirect R&D activities will be eligible for R&D reliefs. Staff costs and software expenditure are among the most popular qualifying categories of expenditure for asset managers.

Only staffing costs for directors and employees directly and actively involved in R&D can qualify. Where someone is partly engaged in R&D, their time should be apportioned so that only staffing costs incurred on R&D activities are included. Staff costs may include:

- all emoluments (including bonuses attributable to R&D activities) paid out to the directors or employees other than benefits in kind,

- secondary Class 1 NIC paid by the company and

- contributions to pension funds paid by the company for the benefit of directors and employees.

For the costs to be deductible, a member of staff must be either a direct employee or an externally-provided worker, meeting the necessary criteria. Directors’ costs can only qualify for R&D relief (where they are carrying out relevant R&D) if they are directly employed by the company.

Software qualifies for R&D when it is incurred and employed directly in carrying out relevant R&D activities, e.g. to record results. Where only part of the cost incurred relates directly to R&D, the expenditure should be appropriately apportioned between R&D and non-R&D activities.

Qualifying expenditure will only be eligible for relief if payment is actually made. While it need not have been made in the accounting period in which the expenditure was incurred, it must have been made before the claim can be valid.

Two new categories of expenditure are introduced from 1 April 2023: the costs of data licenses and cloud computing services. A data licence is defined as one to access and use a collection of digital data. Cloud computing services include providing access to, and maintenance of, remote data storage, operating systems, software platforms and hardware facilities.

Types of R&D relief

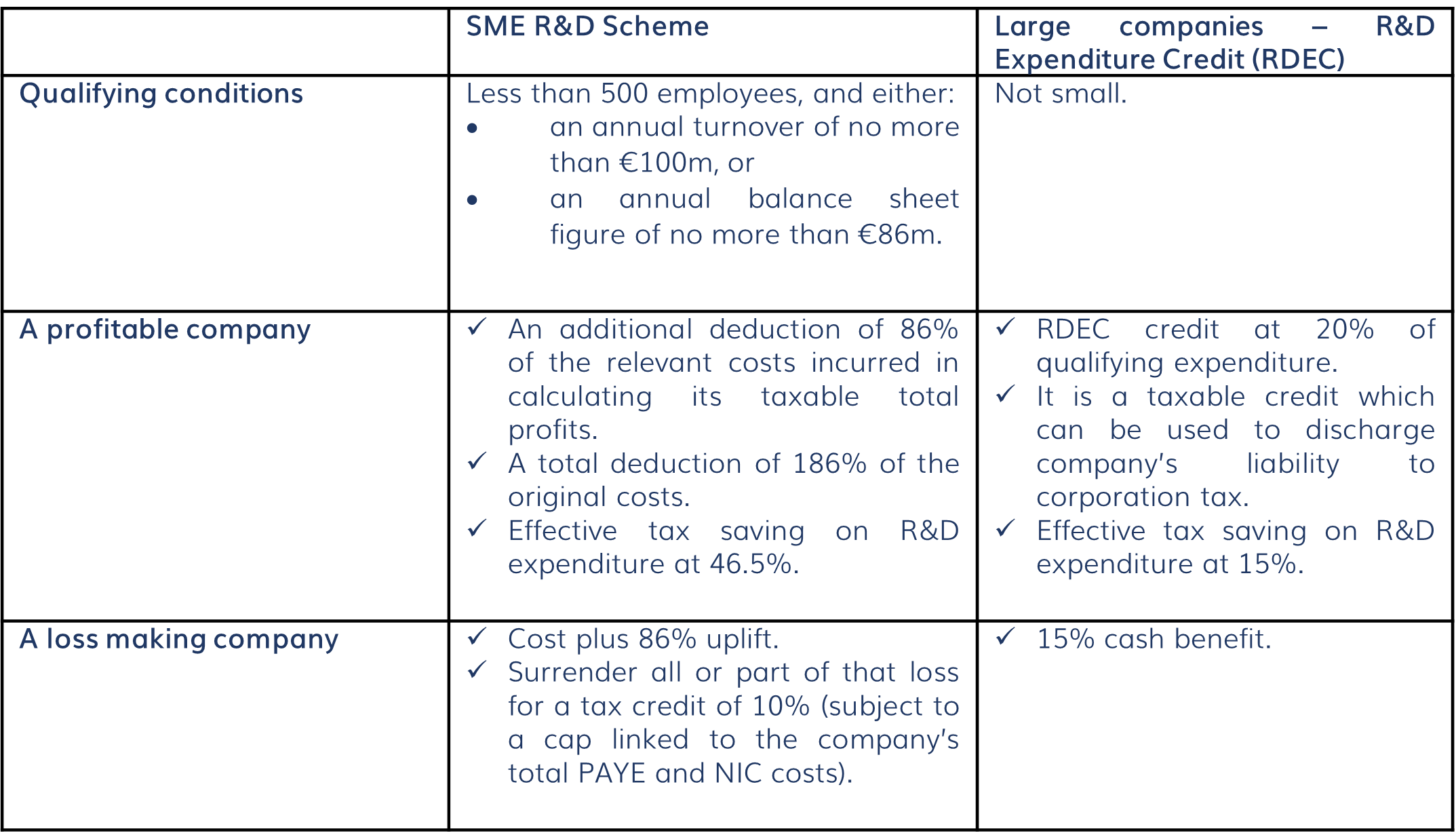

A trading company can tax deduct revenue expenditure against the profits of the trade and capital expenditure may be eligible for a 100% R&D allowance. There are two types of additional R&D reliefs and the type depends on whether the company is a small medium-sized enterprise (SME) or a large company.

From 1 April 2023, a loss making SME which is R&D intensive (at least 40% of the SME’s total expenditure relates to R&D) qualifies for an increased rate of the repayable tax at 14.5%. Relief will be claimed as normal on the return, but on the additional information form (see below) companies should indicate whether or not they are claiming as R&D intensive companies.

From 1 April 2023, a loss making SME which is R&D intensive (at least 40% of the SME’s total expenditure relates to R&D) qualifies for an increased rate of the repayable tax at 14.5%. Relief will be claimed as normal on the return, but on the additional information form (see below) companies should indicate whether or not they are claiming as R&D intensive companies.

Administrative changes from 1 April 2023

For accounting periods beginning on or after 1 April 2023 companies which are making their first R&D claims or have not claimed in the past three years before the last date of the claim notification period or have claimed for the previous tax year, but did not submit that claim until after the last date of the claim notification period (the claim notification period ends 6 months after the end of the period of account) are required to notify HMRC in advance of their plan to claim R&D tax relief. The claim notification form should be completed and submitted online by logging in to HMRC website via a Government Gateway or by using an email address. An agent acting on behalf of the company or a representative of the company can submit the claim notification form. If a company submitted the claim notification form it is required to put an ‘X’ in box 656 of the company tax return to notify HMRC.

From 1 August 2023 companies claiming R&D tax relief or expenditure credit must complete and submit an additional information form to HMRC to support all their claims (irrespective of whether that claim relates to an accounting period beginning before 1 April 2023). The additional information form should be sent before or at the same time company’s corporation tax return is submitted. If this is not done, then HMRC will remove company’s claim for R&D tax relief from the relevant company tax return. It is possible to submit the additional information form before 1 August 2023 if a company wants to give HMRC more information, in this scenario an ‘X’ should be put in box 657 of the company tax return to notify HMRC that an additional information form has been submitted. An agent acting on behalf of the company or a representative of the company can submit the additional information form by signing in using Government Gateway portal. HMRC provides quite an extensive list of information that will be required for this form, including details of R&D projects and breakdown of qualifying expenditure costs.

In addition to the above companies are required to complete and submit a supplementary form CT600L.

The additional submissions set out above will not replace R&D reports with supplementary information to support the R&D claims that are usually drafted and submitted by advisors. HMRC confirmed in the past that these reports may help HMRC to process R&D claims quicker.

Conclusion and what is next?

HMRC continues to scrutinise R&D claims with a number of enquiries spiking. It is imperative for asset managers with existing or new R&D claims to ensure that their R&D related submissions to HMRC satisfy all the requirements. Record keeping is the key as during enquiries HMRC seeks evidence of R&D projects, such as planning/project management documentation, accounting records, R&D staff time sheets, meeting minutes etc.

Further change on the radar for R&D businesses is the proposed single, simplified R&D tax relief scheme, as HMRC consulted to merge the existing RDEC and the SME R&D relief. The consultation closed on 13 March 2023 and we are awaiting further response from HMRC. This proposal is due to be implemented from 1 April 2024.