Despite weeks of rumours and uncertainty, the headline message was that Labour have (claimed) to have kept their manifesto promise not to increase income tax, National Insurance Contributions (NIC) or VAT. The fiscal drag trick of freezing tax bands was once again deployed as a key revenue generator along with an array of smaller changes that will take some time to digest.

For asset managers, the Budget reflects continued tightening around personal tax leakage, corporate deductions and HMRC scrutiny, but the broad conclusion is likely to be that the Budget announcements (or lack of them) are generally welcomed and that it could have been a lot worse.

Despite suggestions of placing an equivalent of employer’s NIC (estimated as 6.9%) on LLPs was to be introduced, this proposal was dropped. This was a real concern for many UK asset managers where the LLP model is extremely popular, albeit it does have a number of restrictions.

The rumour mill was rife with speculation that the UK government would introduce an exit tax or wealth tax, something that could have made a material impact on the UK’s tax competitiveness, particularly for asset managers. Fortunately, these did not feature in the Chancellor’s Budget proposals which is likely to be welcomed by the industry. However, the high value council tax surcharge on properties valued over £2m from April 2028 will hit many in the industry.

Overall, the Budget signals further alignment of the UK tax system with long-term revenue sustainability. Asset managers should prepare for a tighter compliance environment but be thankful that the impact on the industry as a whole is limited, allowing them to focus on the business.

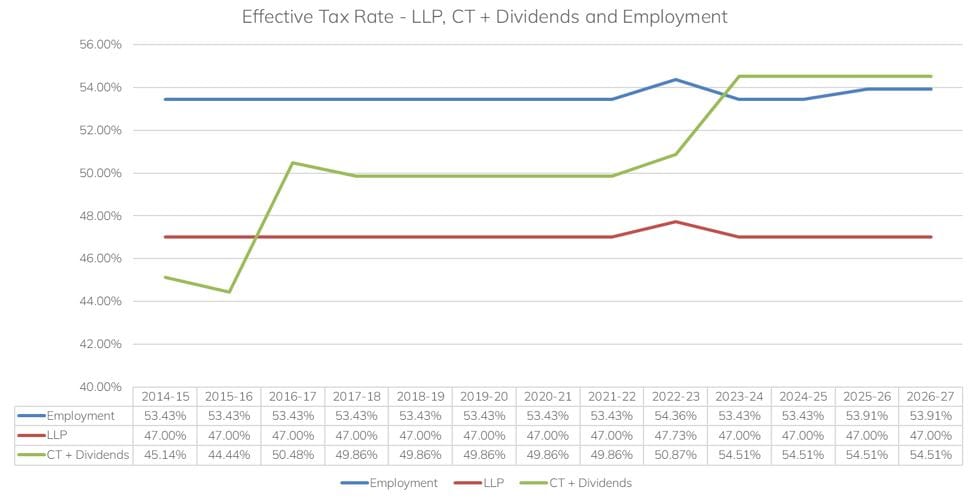

LLP vs Ltd

UK asset managers will continue to look at the comparison in effective tax rates between LLP and Ltd structures. Rates for 2026-27 remain static, a welcome outcome after all the rumours prior to the Budget. The LLP remains the most beneficial for pure profit extraction, but the optionality and planning opportunities afforded by Ltd company structures continue to be appealing for mature managers.

The Salaried Members BlueCrest case is due to be heard at the Supreme Court in January 2026. Asset managers that operate though LLPs should continue reviewing their position with regards to application of the Salaried Members rules as further scrutiny by HMRC is expected.

Dividends

From 6 April 2026, there will be a 2% increase in the ordinary and upper rates of Income Tax applicable to dividends. The additional rate will remain unchanged at 39.35%.

Dividends received above the Dividend Allowance will be taxed at the following rates for 2026/27:

- 10.75% for basic rate taxpayers

- 35.75% for higher rate taxpayers

- 39.35% for additional rate taxpayers.

Overall, it is an interesting move from the Chancellor to retain the additional rate at 39.35% while increasing the lower tax bands. As a consequence the highest effective tax rate remains the same for asset managers that extract profits via dividend distributions – a key comparative as highlighted in the table above.

Capital Gains Tax

There were no further changes to capital gains tax, which will be welcomed across the asset management industry. A further increase in capital gains tax rates would have had an impact on the benefits of the UK’s reporting fund status regime. Nonetheless, managers should continue to review their position and model the impact based on forecast excess reportable income. Further proposed amendments to certain capital gains tax reliefs have been set out below.

Incorporation relief: the government will introduce a requirement for taxpayers to actively claim incorporation relief for transfers of a business to a company on or after 6 April 2026. The relief previously applied automatically. This raises the risk profile for LLPs transferring assets to a corporate structure and individual members claiming incorporation relief.

Employee Ownership Trusts (EOT): the government will reduce the Capital Gains Tax relief available on qualifying disposals to EOT from 100% of the gain to 50%. This will take effect from 26 November 2025.

Business Asset Disposal Relief: the rate applying for individuals claiming Business Asset Disposal Relief and Investors’ Relief will increase to 18% for disposals made on or after 6 April 2026. This relief will not be available on the sale to an EOT.

Reorganisation relief: legislation will be introduced in Finance Bill 2025-26 amending the anti-avoidance provisions that apply to reorganisations, so that they now apply to those cases where a person has entered into arrangements where the main purpose, or one of the main purposes, of those arrangements was to secure them a tax advantage. Where this is satisfied, the reorganisation provisions will not apply. Asset managers should note that clearance applications submitted to HMRC under section 138 before this date will be reviewed under transitional rules. This may hamper efforts by asset mangers to insert holding company structures.

Non-resident capital gains (NRCG): Legislation will be introduced in Finance Bill 2025-26 amending the non-resident capital gains property richness test, so that in the case of Protected Cell Companies (PCCs), a type of company made up of a number of separate cells where the assets and liabilities of one cell are segregated and protected from those of the other cells, it is each individual PCC cell that that is to be looked at for property richness purposes, rather than the PCC as a whole. In addition, an Extra-Statutory Concession that applies to non-UK resident individuals who have invested in Collective Investment Vehicles and exempts them from the requirement to make a double taxation treaty claim by return will be formalised.

Corporation Tax

The government has confirmed that the rates of Corporation Tax will remain unchanged, which means that, from April 2026, the rate will stay at 25% for companies with profits over £250,000. The 19% small profits rate will be payable by companies with profits of £50,000 or less. Companies with profits between £50,001 and £250,000 will pay tax at the main rate reduced by a marginal relief, providing a gradual increase in the effective Corporation Tax rate.

The penalty for taxpayers submitting a Corporation Tax return late will double for returns for which the filing date is on or after 1 April 2026.

The 2% increase in dividend taxation will impact profit extraction from corporate entities. Companies should revisit personal tax modelling and distribution timing. There may be increased appetite for businesses moving away from Ltd structures to LLP structures where pure profit extraction is a priority, but where managers wish to keep value in the business a Ltd structure is likely to remain popular.

Savings Income

Savings income is income such as bank and building society interest. The current tax rates on savings income will be maintained for 2026/27. From 6 April 2027, there will be a 2% increase in the applicable tax rates. The basic rate will increase to 22%, the higher rate will increase to 42% and the additional rate will increase to 47%

The Starting Rate for Savings will be retained at £5,000 for 2026/27 and will stay at this level until 5 April 2031.

Mansion Tax

The government will introduce the High Value Council Tax Surcharge (HVCTS), a new charge on owners of residential property in England worth £2 million or more, starting in 2028/29.

The HVCTS will be staggered depending on the value of the property. The current Council Tax system uses property values from 1991. For property over £2 million, the annual charge will be £2,500. For property valued between £2.5 – £3.5 million, the annual charge will be £3,500 and for those properties valued between £3.5 – £5 million, the annual charge will be £5,000. Properties valued in excess of £5 million will have an annual charge of £7,500.

The surcharge will be collected alongside the existing Council Tax due for the property.

Property Income Tax

From April 2027, the government is creating separate tax rates for property income (any income from letting land and buildings). The separate rates mean property income will have its own individual tax rates (as already occurs for the taxation of savings and dividend income).

The new separate tax rates from 2027/28 are:

- 22% for basic rate taxpayers

- 42% for higher rate taxpayers

- 47% for additional rate taxpayers.

Individuals will have a Property Allowance. This exempts property income of £1,000 or less. Property income over £1,000 can be offset either by the £1,000 Property Allowance or by deducting relevant expenses.

No changes SDLT were announced as part of the Budget.

Business Schemes

The government has announced significant changes to the limits applying to the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCTs) from 6 April 2026.

The gross assets requirement that a company must not exceed for EIS and VCTs will increase from £15 million to £30 million immediately before the issue of the shares, and from £16 million to £35 million immediately after the issue. The annual investment limit that companies can raise will increase from £5 million to £10 million. For Knowledge-Intensive Companies (KICs), the annual investment limit will increase from £10 million to £20 million. The company’s lifetime investment limit will increase to £24 million and for KICs to £40 million. The Income Tax relief that can be claimed by an individual investing in VCTs will decrease from 30% to 20%.

The government is also increasing certain limits relating to the Enterprise Management Incentives (EMI) scheme. For EMI contracts granted on or after 6 April 2026, the employee limit will increase from 250 employees to 500 employees, the gross assets test will be increased from £30 million to £120 million, and the company share option limit will be increased from £3 million to £6 million. The limit on the exercise period will increase to 15 years and will also apply retrospectively to existing EMI contracts which have not already expired or been exercised.

National Insurance Contributions

No changes have been announced to the NICs for the self-employed who are members of Limited Liability Partnerships.

The Primary Threshold, Secondary Threshold, Lower Profits Limit, Upper Earnings Limit (UEL) and Upper Profits Limit for NICs will be maintained at their current levels until April 2031 as well as other employer NICs relief thresholds aligned with the UEL.

The Lower Earnings Limit (LEL), Small Profits Threshold (SPT) and the rates of voluntary Class 2 and Class 3 contributions will be increased by 3.8% from 2026/27.

The rates for Class 4 self-employed NICs remain the same for 2026/27 at 6% and 2%.

In addition, from 6 April 2026, the government will remove access for non-residents to pay voluntary Class 2 NICs although more expensive Class 3 contribution can be made. To be able to pay Class 3 the individual must have lived in the UK for 10 years in a row or have paid 10 years NIC contributions while in the UK.

Carried Interest

From April 2026, all carried interest will be taxed within the income tax framework. A multiplier of 72.5% will be applied to any qualifying carried interest brought within the charge. Draft legislation has been the subject of ongoing consultation but we expect to see an updated version in the draft Finance Bill in the coming weeks.

Income Tax

Regardless of their prior promise not to extend the freeze of the Income Tax Personal Allowance, higher rate threshold and additional rate threshold the government extended the freeze from April 2028 to April 2031.

The basic rate of income tax remains at 20%, the higher rate at 40% and the additional rate at 45%.

The basic rate band remains at £37,700, with the higher rate threshold remaining at £50,270. The additional rate threshold remains at £125,140. The freeze of these thresholds will continue until April 2031. The NICs Primary Threshold and Lower Profits Limit remain at £12,570. The NICs Upper Earnings Limit and Upper Profits Limit will remain aligned to the higher rate threshold at £50,270 up to April 2031 as well. Other employer NICs relief thresholds aligned to the Upper Earnings Limit will also be maintained at this level.

The income tax personal allowance and basic rate limit are £12,570 and £37,700 respectively and will remain frozen until April 2031.

There is a reduction in the personal allowance for those with ‘adjusted net income’ over £100,000. The reduction is £1 for every £2 of income above £100,000. This means that there is no personal allowance where adjusted net income exceeds £125,140. This reduction remains unchanged.

Transfer Pricing / PE / DPT

The government is introducing a package of legislation in respect of the UK’s rules on transfer pricing, Permanent Establishment (PE), and Diverted Profits Tax (DPT).

Transfer Pricing: changes to the transfer pricing legislation has been designed to simplify the UK transfer pricing rules in a number of areas including the participation condition, intangibles, commissioners’ sanctions, UK-to-UK transfer pricing, interpretation in accordance with Organisation for Economic Co-operation and Development (OECD) principles and financial transactions.

Furthermore, the government is introducing legislation to give HMRC the power to introduce regulations requiring in-scope multinationals to file an international controlled transactions schedule (ICTS). The ICTS is expected to be an annual filing requirement that captures specific information about cross-border related party transactions in a standardised format. The information will be used for automated risk profiling and manual risk assessment by HMRC. Given the potential for HMRC to look back into prior years it would be sensible for asset managers to review existing transfer pricing policies now and invest resources where necessary.

A technical consultation on draft regulations will be held in Spring 2026 with changes intended to take effect for accounting periods beginning on or after 1 January 2027. The ICTS limit is not yet decided but is suggested that it should be around £1m aggregate value of cross border transactions (i.e. substantially below the Small and Medium sized Enterprises (SME) limit). Asset managers (many of whom may be able to operate within the SME) will now need to turn their attention to this – noting that HMRC have an array of legislation beyond basic transfer pricing rules to challenge pricing methodologies. This is a hot topic that should be monitored closely.

Separately, consultation responses have also been published on the SME exemption which will be retained, and SMEs will continue to benefit from the existing exemption from transfer pricing.

Permanent establishment: a measure is being introduced to bring the UK’s PE rules into line with the latest international consensus on both the definition of a PE and the attribution of profits to a PE. It will also clarify which supporting guidance and materials can be used in conjunction with UK legislation. A new mechanism will also be introduced for a PE to claim relief when a transfer pricing adjustment is made to a connected UK company.

Diverted Profits Tax: this provision creates a new charging provision for Unassessed Transfer Pricing Profits within Corporation Tax. This is a significant simplification, repealing DPT, which is currently a standalone tax, in its entirety while retaining the essential features of the regime.

The government has published finalised legislation on the above, following a technical consultation on draft legislation at ‘Tax update spring 2025: simplification, administration and reform (TUSAR)’ with the legislation applying to chargeable periods beginning on or after 1 January 2026.

Investment Manager Exemption (IME)

In a move to simplify and clarify the legislation, the government confirmed the following changes to the IME provisions for accounting periods beginning on or after 1 January 2026:

- the removal of the ‘if, and only if’ construction of the IME to ensure that it acts as a safe harbour and not as a mandatory alternative to the general agent exemption;

- the revision of the scope of the IME to cover a wider range of transactions conducted within a fund;

- the inclusion of ‘investment advisors’ such that the rules equally apply to advisors and managers; and

- the highly anticipated removal of Condition D, ‘the 20% rule’, which has caused practical difficulties for asset managers, and which does not serve a clear purpose as an indicator of independence.

UK asset managers should review their IME risk assessment in line with these changes.

OECD Pillar 2

Multinational Top-up Tax and Domestic Top-up Tax are the UK’s adoption of the Pillar 2 Global Anti-Base Erosion (GloBE) rules, agreed by the UK and other members of the OECD and G20 Inclusive Framework on base erosion and profit shifting.

This measure makes amendments identified from stakeholder consultation or otherwise necessary to ensure the UK’s legislation remains consistent with the commentary and administrative guidance to GloBE rules developed by the UK and other members of the Inclusive Framework.

Most provisions in this measure will take effect for accounting periods beginning on or after 31 December 2025, though most will also be permitted to take effect from an earlier date at the election of affected taxpayers.

However, the changes to the treatment of pre-regime deferred tax assets will take effect for accounting periods ending on or after 21 July 2025. Multinational groups with annual global revenues exceeding 750 million euros that have business activities in the UK will be affected.

Making Tax Digital

The government is committed to delivering Making Tax Digital for Income Tax Self Assessment, which starts in April 2026 for those with qualifying income over £50,000. The government will expand the rollout of the programme to those with incomes over £30,000 in April 2027 and £20,000 in April 2028. However, the government will not proceed with Making Tax Digital for Corporation Tax.

Payrolling Benefits

The government confirmed that the use of payroll software to report and pay tax on benefits in kind will become mandatory, in phases, from April 2027. This will apply to income tax and Class 1A NICs. Existing payroll software available in the market support payrolling benefits already, however, so far this has been voluntary.

Capital Allowances

The government will introduce a new 40% First Year Allowance (FYA) for main rate expenditure (including most expenditure on assets for leasing and expenditure by unincorporated businesses) from 1 January 2026. From 1 April 2026 for Corporation Tax and 6 April 2026 for Income Tax, main rate writing down allowances will reduce from 18% to 14%.

Reduced writing down allowances will increase ongoing tax costs for capital spends, but the impact is relatively small and will be spread over a number of years so not a priority for the industry.

For businesses with chargeable periods which span 1 April or 6 April, a hybrid rate will apply. The WDA on the special rate pool will remain at 6% per year.

The Annual Investment Allowance is available to both incorporated and unincorporated businesses. It gives a 100% write-off on certain types of plant and machinery up to certain financial limits per 12-month period. The limit for this will remain at £1 million.

The government will extend for a further year the 100% FYA for qualifying expenditure on zero emission cars and electric vehicle (EV) charge points until 31 March 2027 for corporation tax purposes and 5 April 2027 for Income Tax purposes.

Research & Development

The government will pilot a targeted advance assurance service from spring 2026. This will enable small and medium-sized enterprises to gain clarity on key aspects of their Research and Development (R&D) tax relief claims before submission to HMRC. A summary of responses to the advance clearance consultation will also be published.

Crypto Asset Reporting

The Cryptoasset Reporting Framework (CARF) enables cross-border information exchanges between tax authorities on the transactions of users of crypto assets. The CARF requires UK Reporting Cryptoasset Service Providers (RCASPs) to collect tax relevant information and undertake due diligence in relation to their users on an annual basis from 1 January 2026.

The CARF was implemented to support the successful Common Reporting Standard (CRS) which allows tax authorities to exchange information about financial accounts. This measure ensures that HMRC will have CARF data on all UK taxpayers using both UK based and non-UK based RCASPs. HMRC will receive this standardised, structured data which is required on an annual basis.

Pensions

With no changes announced to the tax regime for pension contributions, limits for 2026/27remain as:

- The Annual Allowance (AA) is £60,000.

- Individuals who have ‘threshold income’ for a tax year of greater than £200,000 have their AA for that tax year restricted. It is reduced by £1 for every £2 of ‘adjusted income’ over £260,000, to a minimum AA of £10,000.

- The Lump Sum Allowance, which relates to the general maximum that may be able to be taken as a tax-free lump sum, is £268,275.

- The Lump Sum and Death Benefit Allowance, which relates to the general maximum that may be able to be taken as a tax-free lump sum in certain circumstances, is £1,073,100.

The government will charge employer and employee NICs on pension contributions above £2,000 per annum made via salary sacrifice. This will take effect from 6 April 2029. Contributions through salary sacrifice, like all pension contributions, will still be exempt from Income Tax (subject to the usual limits). Employers and employees can still make contributions above £2,000 through salary sacrifice arrangements. However, employee contributions above this amount will be subject to employer and employee NICs like other employee workplace pension contributions.

The removal of the NI advantage on pension salary sacrifice increases effective remuneration costs. However, this is relatively minor for many asset managers and pension tax relief is already extremely limited or additional rate taxpayers.

Individual Savings Accounts

For 2026/27, the limits are as follows:

- Individual Savings Accounts (ISAs) £20,000 (cash limit will be set at £12,000).

- Junior ISAs £9,000

- Lifetime ISAs £4,000 (excluding government bonus)

- Child Trust Funds £9,000.

These limits will remain frozen until 5 April 2031. Savers over the age of 65 will continue to be able to save up to £20,000 in a cash ISA each year.

Inheritance Tax (IHT)

In relation to IHT, the government announced that:

- the nil rate band (£325,000), residence nil rate band (£175,000), including its £2m taper limit, will be frozen for a further year, to 5 April 2031;

- the forthcoming combined allowance for the 100% rate of agricultural property relief and business property relief will also be fixed at £1 million for a further year until 5 April 2031. Any unused £1 million allowance will be transferable between spouses and civil partners from 6 April 2026;

- the introduction of a £5m cap on IHT 10 year and exit charges, over each 10-year cycle, for trusts which held excluded property at 30 October 2024, provided that the property remains outside of the UK at the date of each charge;

- the introduction of anti-avoidance measures for non long-term residents and trusts and those gifting to charitable trusts which are not charities.

From 6 April 2027, unused pension funds and death benefits will be included in a person’s estate for IHT. Personal representatives will be liable for any IHT due, though beneficiaries of registered schemes may request administrators to pay HMRC directly or withhold up to 50% of taxable benefits for 15 months.

Company Cars

The government has confirmed increases to the benefit in kind rates for company cars for tax years up to and including 2029/30.

In addition, the government is amending the benefit in kind rules so that vehicles provided through employee car ownership arrangements will be deemed to be taxable benefits when made available on restricted terms.

The government will delay changes to benefit in kind rules for Employee Car Ownership Schemes until 6 April 2030.

VAT

With no changes to VAT rates or registration thresholds, the government made a few announcements with regards to VAT:

- from April 2029 businesses will be required to issue all VAT invoices as e-invoices, with a roadmap on implementation to be published next year.

- the rules relating to operating cross border VAT grouping are further clarified and apply from 26 November 2025.

- a new VAT relief for business donations of goods to charity will take effect from 1 April 2026.

- from 1 April 2027 higher late payment penalties will apply for VAT.

Enforcement and Tax Collection

The government has announced a series of compliance initiatives aimed at closing the UK tax gap. HMRC will receive additional investment to strengthen debt management, supported by a new tax debt strategy targeting year‑on‑year reductions in outstanding liabilities.

From April 2029, Self Assessment taxpayers with PAYE income will be required to settle more of their liabilities in‑year via PAYE, tightening cash‑flow management for affected individuals.

Significant investment will also be directed toward modernising the tax system. HMRC plans to expand digitalisation, improve use of third‑party data, and introduce data‑driven prompts to reduce errors in tax returns.

These measures are expected to raise an additional £10 billion by 2029/30, reflecting a more assertive compliance environment. At the same time, the government is consulting on the effectiveness of existing tax incentives for business founders and scaling firms, with the aim of ensuring the UK remains competitive for growth and investment.

For asset managers, the key takeaway is the need to prepare for tighter compliance and increased digital reporting.

Post Departure Trade Profits

The Temporary Non-Residence Rules (TNR) are designed to prevent individuals from adopting non-resident status for tax‑motivated reasons, thereby avoiding UK Income Tax and Capital Gains Tax.

Under the current framework, no UK tax charge arises where a distribution or dividend is paid out of post‑departure trade profits – that is, profits accruing to a company after the individual has left the UK. The proportion of a dividend or distribution attributable to such profits is determined on a “just and reasonable” basis.

The new measure abolishes the concept of post‑departure trade profits within the TNR regime.

As a result, all distributions or dividends received from a close company during a period of temporary non‑residence will be subject to UK income tax if the TNR rules apply. This change will affect individuals returning to the UK on or after 6 April 2026.

In addition, new legislation will be introduced to further provisions aimed at preventing tax avoidance through the use of offshore structures and arrangements.

Mandatory Tax Advisor Registration

From May 2026 tax advisers who interact with HMRC on behalf of clients will be legally required to register and meet minimum standards before doing so.

As part of a wider package to raise standards in the tax advice market and reduce the tax gap, HMRC are introducing the following measures

- changes allowing HMRC to request information from tax advisers where there is reasonable suspicion of sanctionable conduct;

- penalties for tax advisers who engage in sanctionable conduct, calculated based on the tax loss;

- a new power allowing HMRC to publish details of advisers where they have been sanctioned.

Umbrella Companies

To tackle the significant levels of tax avoidance and fraud in the umbrella company market, the government will make recruitment agencies responsible for accounting for PAYE and Class 1 NICs on payments made to workers that are supplied via umbrella companies.