The asset management industry enters 2026 on a high, fuelled by strong performance in 2025 and the steady inflows of capital. But momentum alone is not enough: this is the year when tax shapes strategy. From cross‑border rules to carried interest reforms, tax decisions now sit at the heart of how UK asset managers scale, attract talent and protect competitiveness. With this in mind, we look at the key areas of UK taxation that are likely to impact the asset management industry in 2026.

“Salaried Member” Risk and the BlueCrest Litigation

Asset managers operating through LLP structures should continue to assess their exposure under the salaried member rules, particularly in light of the BlueCrest Case, heard at the Supreme Court in January 2026. HMRC’s argument on Condition A was that variable allocations must be genuinely calibrated to the LLP’s overall profits/losses – the mere fact of that the remuneration might be capped by the overall amount of profits does not convert the remuneration mechanism to be within the rules. On Condition B, HMRC’s arguments revolved around member’s contractual and statutory rights, ‘influence’ interpreted as formal decision making or authority rather than the financial impact that members might happen to make, ‘significant’ influence as influence of practical and commercial substance and judged relative to the size of the LLP’s affairs; and ‘affairs’ to be viewed in light of strategic influence or influence at the management level.

A judgment may take up to six months. Until then, HMRC is expected to continue applying the Court of Appeal decision.

We also note that HMRC is conducting a survey via IFF Research and letters have been sent to selected group of individual members regarding taxation of their LLPs. The questions in the survey specifically focus on salaried members and mixed members. Survey’s notes state that it is confidential, but we advise to exercise caution and for the LLPs to proactively reach out to their members to confirm if they have received such a letter.

Immediate Action Points

- Evidence Condition A: Revisit the disguised salary test to confirm that variable profit allocations remain linked to overall LLP profitability. This must be done at the beginning of each relevant period, when remuneration arrangements change or when new members join the LLP. It is a forward looking test, and LLPs with 31 March year end are advised to conduct their analysis in advance of the new fiscal period.

- Document Condition B: Ensure analysis with respect to each partner’s significant influence rights are documented and expressed appropriately in the LLP Agreement and reflected in committee or board terms of reference.

- Record Condition C: Where relevant, document capital contributions and capital at risk. This condition needs to be tested a t the beginning of each tax year and in addition, whenever there is a change in the contribution, or there is, otherwise, a change in circumstances that might affect whether or not Condition C is met.

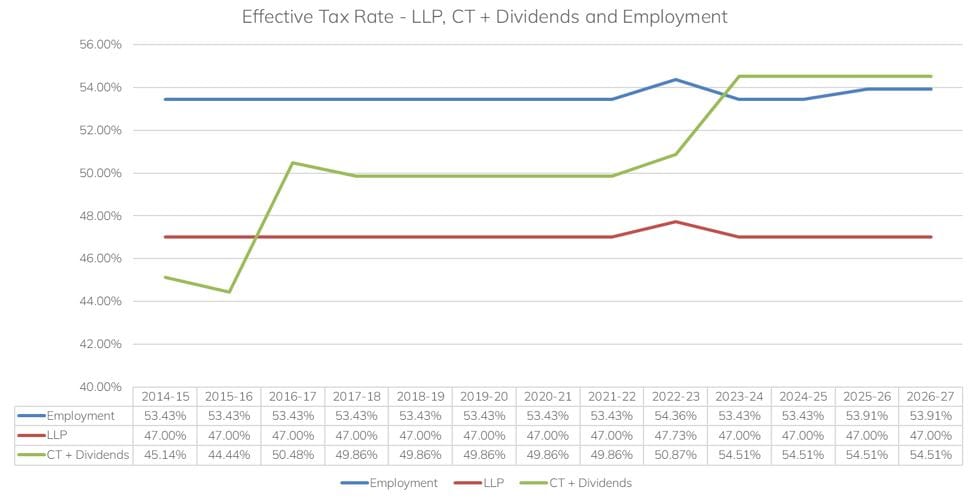

LLP vs Ltd in 2026/27: Rates Steady, but Behaviours Are Shifting

With the Autumn Budget 2025 keeping most headline rates stable for 2026/27 – aside from a 2% increase in dividend ordinary and upper rates from 6 April 2026 (to 10.75% basic and 35.75% higher, with the 39.35% additional rate unchanged) – the long‑standing comparison between LLP and Ltd structures remains highly relevant for UK asset managers.

LLPs continue to offer the most efficient route for pure profit extraction, particularly where partners draw profits directly and value flexibility over corporate retention. However, as businesses mature, many are increasingly drawn to the planning opportunities and optionality available under limited‑company structures – including retained‑profit strategies, deferred remuneration structuring, enhanced governance frameworks and corporate‑level investment planning. The result is a shift in behaviour: while LLPs remain optimal for early‑stage or high‑distribution businesses, more established managers are revisiting whether a company structure better supports long‑term growth, institutionalisation and succession planning.

Immediate Action Points

- Run structure comparisons: Model LLP versus Ltd outcomes, including hybrid or phased‑transition models.

- Plan for growth: Consider long‑term capital needs, regulatory capital requirements and reinvestment strategy.

- Stress‑test succession: Review whether the current structure supports generational transitions, staff participation or external investment.

Transfer Pricing (TP) Reform and Heightened HMRC Expectations

The Finance Bill 2025/26 introduces comprehensive modernisation of the UK TP framework effective for periods beginning on or after 1 January 2026. Key reforms include updates to the participation condition, changes to UK–UK TP, closer alignment with OECD TP Guidelines, and replacing the Diverted Profits Tax regime with the new Unassessed TP Profits mechanism. Financial transaction rules are also strengthened, requiring explicit consideration of implicit guarantees and group support when determining arm’s length interest rates.

Asset managers must also prepare for the introduction of the International Controlled Transactions Schedule (ICTS) from 1 January 2027 – an annual filing requiring detailed, standardised disclosures on cross‑border related‑party transactions. ICTS supports both automated and manual HMRC risk assessment and represents a significant step change in HMRC’s enforcement strategy.

HMRC has additionally updated its guidance on common TP risks, including new sections on value chain analysis and offshore procurement hubs, signalling a continued rise in expectations around analytical depth and documentation quality.

Immediate Action Points

- Review cross‑border arrangements: Conduct a comprehensive review of the group structure, intercompany services, and cost allocations.

- Strengthen documentation: Maintain robust TP policy documentation and arm’s length evidence for all material transactions.

- Prepare for ICTS: Begin data‑mapping and compliance planning well ahead of the 2027 implementation date.

- Monitor TP governance: Establish regular policy and risk reviews to identify issues early and ensure operational alignment with TP policies.

Investment Manager Exemption (IME) and Permanent Establishment (PE) Modernisation

From 1 January 2026, the UK has aligned its definition of a PE with the 2017 OECD Model, broadening the concept of a “dependent agent” PE. Concurrently, the IME has been modernised and its scope clarified, including removal of the “20% rule,” widening of “investment transactions,” and clearer interaction with the agent of independent status concept – all aimed at safeguarding the UK’s competitiveness for offshore funds using UK based managers.

Immediate Action Points

- Reassess PE exposure: Review deal sourcing, negotiation and contract conclusion behaviours against the updated PE rules.

- Update IME documentation: Ensure annual IME assessments are documented and reflect all the changes.

- Review fee arrangements: Confirm that investment management and advisory fees remain supportable with arm’s length evidence.

Carried Interest: New Regime from 6 April 2026

From 6 April 2026, carried interest will be taxed entirely within the Income Tax regime as deemed trading profits, subject to Income Tax and Class 4 NICs. Where carried interest is “qualifying,” only 72.5% of the amount is taxable – resulting in an effective rate of roughly 34.1% for additional‑rate taxpayers. “Qualifying” carry is broadly defined as carry not falling under the Income‑Based Carried Interest (IBCI) rules and meeting a weighted average holding period of ≥40 months (with partial relief from 36 months).

The legislation removes the long‑standing exclusion that prevented carried interest treated as employment‑related securities (ERS) from being pulled into the IBCI framework. Also, application of the Disguised Investment Management Fee (DIMF) rules continues to apply in full to determine whether amounts received by investment managers should be recharacterised as trading income rather than carried interest.

For managers relocating abroad, the territoriality rules remain important: carried interest will still be taxable in the UK to the extent linked to UK workdays. The regime includes new definitions of “UK workdays”, covering days spent partly in the UK and relevant travel time, making accurate tracking essential.

Immediate Action Points

- Evaluate carry structures: Map existing carry plans against the new holding‑period rules and DIMF/IBCI interactions.

- Model individual impact: Quantify the financial implications for relevant members of staff.

- Update documentation: Refresh internal documentation that covers carried interest arrangements.

- Ensure cross‑regime alignment: Confirm consistency between carried interest design, transfer pricing arrangements and IME frameworks.

Non‑Dom Overhaul: Life After the Remittance Basis

Nearly one year on from the abolition of the remittance basis, the new regime significantly reshapes planning for internationally mobile professionals. Individuals newly arriving in the UK – or returning after 10 consecutive years of non‑residence – can access a four‑year, 100% exemption on foreign income and gains.

The Temporary Repatriation Facility (TRF) allows pre‑6 April 2025 foreign income and gains to be remitted at 12% (2025/26 and 2026/27) or 15% (2027/28). For asset managers, these changes affect recruitment, mobility planning and structuring of senior staff compensation.

For those planning to leave the UK, the Temporary Non‑Residence Rules (TNR) remain essential: individuals returning within five full tax years risk UK charges on certain offshore income and gains realised while abroad.

Immediate Action Points

- Plan mobility strategies: Incorporate the four‑year FIG exemption into hiring and compensation planning for internationally mobile staff.

- Evaluate TRF opportunities: Identify senior individuals who may benefit from remitting historic offshore income at preferential rates.

- Update tax‑equalisation policies: Adapt internal mobility and secondment policies to the post‑remittance landscape.

- Assess TNR exposure: For departing members of staff, review potential UK tax liabilities if return occurs within five years.